Key Takeaways:

Key Takeaways:

- Not every state gives an oppressed LLC member a statutory remedy. New York and Delaware confine judicial dissolution to the strict “not reasonably practicable” standard; New Jersey’s LLC statute expressly authorizes relief for oppression, and that power cannot be waived in the operating agreement.

- In the gap states, freeze-out conduct alone rarely wins dissolution. The realistic paths are fiduciary duty claims — which produce damages, not exit — and, in New York, a court-fashioned buyout available only after a dissolution claim succeeds.

- The economic stakes travel with the statute. Without a statutory trigger there is no valuation date and no forced liquidity event, and the applicable standard of value — fair value versus fair market value — can move the price of a minority interest by a quarter or more.

- The state of formation controls, not the state of operation. A Delaware-formed LLC running a New Jersey business gives its minority members Delaware remedies.

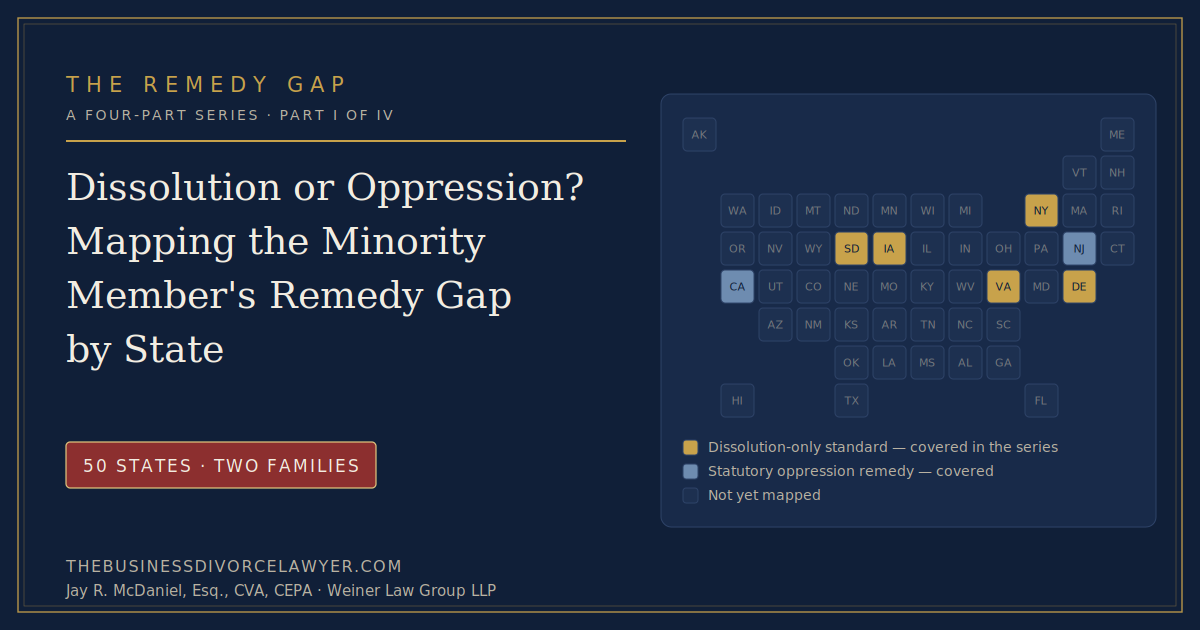

In half the country, a frozen-out LLC member has a statutory oppression claim. In the other half — including New York and Delaware, whose law governs a large share of the closely held entities operating in this region — the statute offers a single remedy, judicial dissolution, on a standard most oppressed members cannot meet. This article maps the divide: which states fall on which side of it, what a minority member is left with when the statute runs out, and why the answer determines not only whether there is a claim but what the membership interest is worth.

Table of Contents

- The Issue: One Statutory Question Decides the Case

- The Doctrinal Landscape: Two Families of LLC Statutes

- Where the Remedy Gap Exists — and What Fills It

- Valuation and Economic Consequences

- Case Law Digest

- Practical Guidance: A Decision Path

- FAQs

- Related Resources

1. The Issue: One Statutory Question Decides the Case

A minority LLC member is cut off. Distributions stop. The management title disappears. The books close. The conduct looks like textbook oppression, and in a corporation it often would be. But the strength of that member’s case turns on a question most owners never ask until it is too late: does the LLC statute in the state of formation recognize oppression as a ground for judicial relief?

The answer determines the entire architecture of LLC minority oppression remedies by state. Roughly half the states — those that adopted the Revised Uniform Limited Liability Company Act or added comparable provisions — give courts express authority to intervene when those in control act oppressively, fraudulently, or illegally. The other half confine judicial dissolution to a single, deliberately narrow ground: that it is “not reasonably practicable” to carry on the business in conformity with the operating agreement. In those states, oppressive conduct that leaves the business running is conduct the dissolution statute does not reach.

One correction to the conventional wisdom before going further. New Jersey is not a remedy-gap state. N.J.S.A. 42:2C-48(a)(5)(b) authorizes a court to dissolve an LLC — or order a lesser remedy — where managers or controlling members have acted “in a manner that is oppressive and was, is, or will be directly harmful to the applicant.” An oppressed member of a New Jersey LLC has a statutory claim, and it is one of the few provisions of the New Jersey act that an operating agreement cannot eliminate. N.J.S.A. 42:2C-11(c)(7).

The remedy gap matters to New Jersey owners and their counsel for two reasons. First, closely held businesses operating here are frequently formed in Delaware, and the law of the state of formation governs the members’ internal affairs. Second, cross-border disputes with New York members and New York entities are routine in this market. When the entity is Delaware-formed or New York-governed, the New Jersey oppression playbook does not travel with it.

2. The Doctrinal Landscape: Two Families of LLC Statutes

The contractarian family: dissolution only, strictly construed

Delaware wrote the template. Under 6 Del. C. § 18-802, the Court of Chancery may dissolve an LLC whenever it is not reasonably practicable to carry on the business in conformity with the LLC agreement. That is the only statutory ground. There is no oppression provision, no deadlock provision, no unfairness provision. Delaware courts construe the standard narrowly and grant the remedy rarely, treating the LLC as a creature of contract whose members are held to the exit rights they negotiated — or failed to negotiate.

New York follows. LLC Law § 702 uses materially identical language, and the Second Department’s decision in Matter of 1545 Ocean Avenue, LLC, 72 A.D.3d 121 (2d Dept. 2010), fixed its meaning: the petitioner must show either that management is unable or unwilling to permit the LLC’s stated purpose to be achieved, or that continuing the entity is financially unfeasible. Member discord does not qualify. The court expressly rejected a divorce-style equitable standard.

New York courts have since refused every invitation to soften the rule. In Kassab v. Kasab, 195 A.D.3d 830 (2d Dept. 2021), a member alleged exclusion from management — conduct that would state an oppression claim under Business Corporation Law § 1104-a. The court held the allegations insufficient under § 702, describing the LLC standard as more stringent than the corporate one and declining to import BCL oppression doctrine into the LLC Law. Exclusion from management, standing alone, does not establish that the business cannot practicably continue.

Virginia sits in the same family. In Dunbar Group, LLC v. Tignor, 267 Va. 361 (2004), the Virginia Supreme Court reversed a dissolution order entered on deadlock facts, calling the statutory standard a strict one and requiring proof that the LLC genuinely could not continue to operate.

The flexible family: oppression and misconduct as express grounds

New Jersey’s Revised Uniform Limited Liability Company Act, effective 2013 and applicable to all New Jersey LLCs since March 2014, carried the corporate oppression remedy into the LLC statute. N.J.S.A. 42:2C-48(a)(5) authorizes dissolution on a member’s application where those in control have acted illegally or fraudulently, or oppressively and directly harmfully to the applicant. Subsection 48(b) authorizes remedies short of dissolution — the practical foundation for court-ordered buyouts. The architecture has a drafting wrinkle worth knowing: the court’s power to dissolve for oppression cannot be waived, N.J.S.A. 42:2C-11(c)(7), but under the uniform act’s official comment the lesser-remedy power of subsection (b) can be restricted by the operating agreement — members may confine the court, and themselves, to the all-or-nothing remedy of dissolution. Few agreements address the point. The ones that do are making a leverage decision, deliberately or not.

California’s Revised Uniform Limited Liability Company Act takes a different route to a similar place. Cal. Corp. Code § 17707.03(b) lists five dissolution grounds, including that management is deadlocked, that dissolution is reasonably necessary to protect the complaining members, and that those in control are guilty of “persistent and pervasive fraud, mismanagement, or abuse of authority.” Precision matters here: the California LLC statute does not use the word “oppression,” and it omits the “persistent unfairness” ground that appears in the corporate statute, Corp. Code § 1800(b)(4). What California adds instead is procedural: under § 17707.03(c), the non-moving members may avoid dissolution by electing to purchase the petitioner’s interest at fair market value, with court-appointed appraisers fixing the price. Filing for dissolution in California is, functionally, pulling the trigger on a buyout — sometimes the petitioner’s, whether the petitioner wants one or not.

The middle ground: courts stretching the strict standard

A handful of decisions show courts reaching oppression-like results without an oppression statute. In Kirksey v. Grohmann, 754 N.W.2d 825 (S.D. 2008), four sisters owned a ranching LLC in equal shares; two controlled it and shut the other two out of any meaningful role. South Dakota’s statute contained no oppression ground, but the court held the freeze-out made it not reasonably practicable to carry on the business in conformity with an operating agreement built on equal participation. The majority’s conduct had destroyed the governance structure the members contracted for, and that was enough.

The Iowa Supreme Court went the other way on comparable pressure. In Barkalow v. Clark, 961 N.W.2d 195 (Iowa 2021), one member had engaged in self-dealing serious enough to support a damages award. The court nonetheless reversed a dissolution order, synthesizing the case law into three conditions — unbreakable deadlock, failed purpose, or financial infeasibility — and finding none present in a profitable rental-property LLC that the majority continued to run. Dissolution, the court held, is a “drastic remedy,” not a general mechanism for doing equity. Wrongdoing gets damages; it does not get dissolution unless it destroys the company’s ability to function.

Kirksey and Barkalow mark the boundaries of the middle ground. Where majority conduct guts the governance bargain itself, some courts will find the standard met. Where the business still runs in conformity with the agreement — even profitably, even with a wrongdoer at the helm — most will not.

3. Where the Remedy Gap Exists — and What Fills It

For the minority member of a New York or Delaware LLC, the absence of an oppression statute is not the end of the analysis. It is the beginning of a different one. Three theories remain, each with a distinct posture, burden, and economic endpoint.

Theory one: the dissolution claim itself

The claim exists; the standard is the problem. Under 1545 Ocean and § 18-802 doctrine, the petitioner must prove failed purpose or financial infeasibility, measured against the operating agreement.

The cases where petitioners win share a fact pattern. In In re Silver Leaf, L.L.C., 2005 WL 2045641 (Del. Ch. Aug. 18, 2005), the LLC existed to market a specific vending-machine product, the venture had collapsed, the members were locked in a 50/50 impasse, and the agreement provided no tie-breaker. Purpose dead, deadlock total, no contractual escape: dissolution granted. In Haley v. Talcott, 864 A.2d 86 (Del. Ch. 2004), two 50% members of a restaurant-property LLC were deadlocked, and although the agreement contained a buy-sell exit, the court found it inadequate because exercising it would have left the petitioner exposed on a personal guaranty of the LLC’s mortgage. An exit that does not actually release the exiting member does not defeat dissolution.

The cases where petitioners lose share a different one. In In re Arrow Investment Advisors, LLC, 2009 WL 1101682 (Del. Ch. Apr. 23, 2009), and In re Seneca Investments LLC, 970 A.2d 259 (Del. Ch. 2008), the operating agreements authorized any lawful business. When the purpose clause is that broad, almost nothing counts as failed purpose — an entity reduced to passively holding assets still satisfies a charter that permits everything. The Chancery Court will not dissolve an LLC because the business disappointed or the members fell out; it requires a strong showing that continuing the entity is futile.

The control lesson is drafted into every one of these outcomes. A broad purpose clause is a shield for whoever controls the company. A narrow one is a sword for whoever wants out. Members negotiating operating agreements are allocating dissolution leverage whether they know it or not.

One Delaware development cuts the other way and deserves more attention than it gets. In In re Carlisle Etcetera LLC, 114 A.3d 592 (Del. Ch. 2015), the petitioner held its position as an assignee rather than a member and therefore lacked standing under § 18-802. The Court of Chancery held that the statute is not the exclusive path — under 6 Del. C. § 18-1104, equity supplements the act, and the court retains equitable jurisdiction to dissolve where the statutory route is unavailable. Carlisle does not lower the substantive bar, but it confirms that even in the most contractarian jurisdiction, the door to equity is not fully closed.

Theory two: fiduciary duty and the implied covenant

When dissolution fails, breach of fiduciary duty is usually the operative claim — and unlike dissolution, it targets the conduct rather than the entity. In New York, courts apply common-law fiduciary principles to managing members. In Delaware, default fiduciary duties of loyalty and care apply unless the LLC agreement validly modifies or eliminates them, 6 Del. C. § 18-1101(c), and Stone & Paper Investors, LLC v. Blanch, 2021 WL 3925739 (Del. Ch. July 30, 2021), confirms that general duty language short of an unambiguous waiver leaves the defaults intact. Even a full waiver has a floor: § 18-1101(e) preserves liability for bad-faith violation of the implied covenant of good faith and fair dealing.

The fiduciary route changes the remedy profile. It produces damages, disgorgement, and accounting relief — not exit. It can build leverage toward a negotiated buyout, but it does not compel one. The Delaware version of this analysis, including how waiver scope is negotiated at formation, is the subject of a companion piece: When the LLC Agreement Waives Fiduciary Duties: Delaware’s Contract-First Approach to Member Disputes.

Theory three: the court-fashioned buyout

New York has developed a doctrine the statute nowhere mentions: where a dissolution claim succeeds, courts may — and in the right posture must — order a buyout as an equitable method of winding up, even when the operating agreement provides no buyout right. The doctrinal turn came in Mizrahi v. Cohen, 104 A.D.3d 917 (2d Dept. 2013), where the court granted dissolution of a 50/50 real estate LLC on financial-infeasibility grounds and then directed that the plaintiff be permitted to purchase the defendant’s interest following a judicial valuation. The sequencing is essential: the equitable buyout is relief layered onto a winning dissolution claim, not a workaround for a losing one. The doctrine, its lineage, and its valuation mechanics are covered in depth in a companion piece: No Statutory Buyout, No Problem: How New York Courts Order Forced Buyouts in LLC Dissolution Cases.

For the New York member weighing all three theories together — what dissolution requires, why it usually fails on discord facts, and what leverage remains — the state-specific playbook is here: No Oppression Statute, No Forced Exit: The New York LLC Member’s Playbook.

4. Valuation and Economic Consequences

The remedy gap is, at bottom, a valuation problem. Every statutory oppression remedy carries an embedded liquidity event: a finding of oppression triggers a buyout or dissolution, which triggers a valuation date, which converts an illiquid minority interest into a payment obligation. Remove the statute and the chain never starts.

Three economic consequences follow for the minority member in a gap jurisdiction.

Capital becomes hostage capital. Without a forced-exit mechanism, the controlling member sets the timeline. He can suspend distributions, pay himself through salary and related-party transactions, and wait. The minority interest keeps its paper value and loses its economic function. Time is the majority’s asset and the minority’s cost, and the majority knows it.

There is no valuation date until a claim creates one. A fair-value proceeding fixes value as of a statutory moment and typically insulates the oppressed owner from the conduct that destroyed value. A gap-state member gets a valuation date only by winning something — a dissolution decree, a fiduciary judgment with an accounting, a negotiated buyout. Until then, the majority controls not just the company but the measurement.

The valuation standard travels with the statute, and the differences are material. New Jersey oppression remedies operate in a fair-value framework in which marketability and minority discounts are generally disfavored, subject to case-specific equitable adjustment. California’s § 17707.03(c) election uses a different measure: fair market value. In Cheng v. Coastal LB Associates, LLC, 69 Cal. App. 5th 112 (2021), the Court of Appeal affirmed a buyout price that applied a 27% discount to a 25% membership interest, holding that fair market value under the LLC statute is not the fair value of the corporate cases. Same state, same fact family, different entity form — and a quarter of the interest’s undiscounted value gone. In New York, where the equitable buyout doctrine supplies the exit, no statutory valuation standard exists at all for LLCs; the measure of value is itself litigated. The lesson generalizes: the choice of entity and state of formation is also, silently, the choice of what a minority interest will be worth on the way out.

5. Case Law Digest

Current through July 2026. Reviewed quarterly.

Matter of 1545 Ocean Avenue, LLC, 72 A.D.3d 121 (2d Dept. 2010). Controlling New York standard under LLC Law § 702: failed purpose or financial infeasibility, measured against the operating agreement. Rejects member discord as a ground.

Kassab v. Kasab, 195 A.D.3d 830 (2d Dept. 2021). Exclusion from management does not satisfy § 702; the court declines to import BCL § 1104-a oppression doctrine and describes the LLC standard as more stringent.

Haley v. Talcott, 864 A.2d 86 (Del. Ch. 2004). 50/50 deadlock; contractual buy-sell held inadequate because it left the petitioner’s personal guaranty in place; dissolution granted.

In re Silver Leaf, L.L.C., 2005 WL 2045641 (Del. Ch. Aug. 18, 2005). Specific purpose failed, hostile factions deadlocked, no contractual tie-breaker; dissolution granted.

In re Seneca Investments LLC, 970 A.2d 259 (Del. Ch. 2008). Passive asset-holding satisfies an any-lawful-purpose charter; dissolution denied.

In re Arrow Investment Advisors, LLC, 2009 WL 1101682 (Del. Ch. Apr. 23, 2009). Abandonment of the original business plan does not defeat a broad purpose clause; dissolution requires a strong showing of futility.

In re Carlisle Etcetera LLC, 114 A.3d 592 (Del. Ch. 2015). Section 18-802 is not the exclusive route; Chancery retains equitable power to dissolve where statutory standing is unavailable, per § 18-1104.

Dunbar Group, LLC v. Tignor, 267 Va. 361, 593 S.E.2d 216 (2004). Virginia Supreme Court reverses a deadlock-based dissolution; the statutory standard is strict.

Kirksey v. Grohmann, 754 N.W.2d 825 (S.D. 2008). Freeze-out of two of four equal members destroyed the contracted governance structure; standard satisfied without an oppression statute.

Barkalow v. Clark, 961 N.W.2d 195 (Iowa 2021). Three-condition synthesis — deadlock, failed purpose, financial infeasibility; self-dealing supporting damages does not support dissolving a functioning, profitable LLC.

Mizrahi v. Cohen, 104 A.D.3d 917 (2d Dept. 2013). Dissolution granted on financial infeasibility; buyout ordered as equitable relief despite the absence of any buyout provision in the operating agreement.

Cheng v. Coastal LB Associates, LLC, 69 Cal. App. 5th 112 (2021). Fair market value under Cal. Corp. Code § 17707.03(c) permits minority discounts; the fair-value jurisprudence of the corporate buyout statute does not control.

6. Practical Guidance: A Decision Path

Start with the state of formation, not the state of operation. Internal-affairs doctrine means a Delaware-formed LLC running a New Jersey business gives its minority members Delaware remedies. This single fact reroutes the entire analysis, and it is the most common surprise in these engagements.

Read the operating agreement before theorizing. Four provisions carry the case: the purpose clause (broad favors the incumbent; narrow favors the petitioner), any buy-sell or exit mechanism (an adequate one defeats dissolution; an inadequate one, per Haley, does not), any fiduciary duty waiver (and whether it is unambiguous under Stone & Paper), and in New Jersey, any restriction on the court’s lesser-remedy powers under 42:2C-48(b).

Map the claims to the jurisdiction family. In a flexible state, the oppression or misconduct claim leads and dissolution rides along as remedial leverage. In a gap state, invert it: fiduciary and accounting claims carry the merits, and dissolution is pleaded only where the facts genuinely fit failed purpose, infeasibility, or intractable deadlock. A dissolution count that Kassab would dismiss weakens the pleading it sits in.

Fix the valuation posture before filing. Know what standard of value the endgame will apply, what a discount fight is worth in dollars, and whether the filing itself triggers a buyout election — in California, it does, at a discounted measure of value. The economics of the exit should be modeled before the complaint is drafted, not after the remedy is won.

7. FAQs

Does every state have an LLC minority oppression statute?

No. Roughly half the states, including New Jersey and other RULLCA jurisdictions, authorize judicial relief for oppressive conduct by those in control. Delaware, New York, and Virginia do not; their LLC statutes limit judicial dissolution to the “not reasonably practicable” standard, which courts construe strictly.

Is New Jersey a state without an LLC oppression remedy?

No — the opposite. N.J.S.A. 42:2C-48(a)(5)(b) expressly authorizes dissolution or lesser remedies where controlling members act oppressively and harmfully to the applicant, and the operating agreement cannot eliminate the court’s power to dissolve on that ground.

Can a frozen-out member force dissolution of a New York LLC?

Rarely on freeze-out facts alone. Under 1545 Ocean Avenue and Kassab, exclusion from management and member discord do not satisfy LLC Law § 702; the member must show the LLC’s purpose has failed or that continuing it is financially unfeasible.

What does the remedy gap mean for the value of my membership interest?

Without a statutory oppression remedy, there is no automatic buyout trigger and no fixed valuation date, so a minority interest can be starved of distributions indefinitely without a forced liquidity event. Value is realized only through a successful dissolution claim, a fiduciary judgment, or a negotiated exit — and the valuation standard that applies depends heavily on the state and theory of recovery.

Is Delaware’s dissolution standard different from New York’s?

The statutory language is materially the same and both are strict. Delaware adds two features New York lacks: near-total freedom to modify fiduciary duties by contract under § 18-1101(c), and confirmed equitable jurisdiction to dissolve outside the statute under In re Carlisle Etcetera LLC.

Can an operating agreement waive the oppression remedy in a state that has one?

In New Jersey, the court’s power to dissolve for oppression is non-waivable under N.J.S.A. 42:2C-11(c)(7), but the uniform act’s comments indicate the court’s lesser-remedy powers under 42:2C-48(b) may be restricted by agreement — a drafting decision with real leverage consequences that most operating agreements never address.

8. Related Resources

- No Oppression Statute, No Forced Exit: The New York LLC Member’s Playbook

- No Statutory Buyout, No Problem: How New York Courts Order Forced Buyouts in LLC Dissolution Cases

- When the LLC Agreement Waives Fiduciary Duties: Delaware’s Contract-First Approach to Member Disputes

- When to Seek Judicial Dissolution of an LLC

- Minority Shareholder & LLC Member Oppression in New Jersey

If you are a minority member being frozen out of management or distributions — in New Jersey, New York, or a Delaware-formed entity — the remedies available to you, and the value of your interest, depend on decisions that should be made before anything is filed. Schedule a consultation.

If you are litigating a business divorce matter and need valuation counsel — particularly where no statutory valuation standard governs the exit — I work with litigation counsel as a CVA on fair value, fair market value, and discount disputes in member and shareholder cases. Contact for co-counsel and valuation engagements.

Jay R. McDaniel, Esq., CVA, CEPA, is Chair of the Corporate & Business Law practice at Weiner Law Group, leader of its Business Divorce Practice, and founder of Closely Held Advisors.

Attorney Advertising. This article is for informational purposes only and does not constitute legal advice or create an attorney-client relationship. Prior results do not guarantee a similar outcome.